Filing taxes online, or e-filing, has surged in popularity due to its efficiency and convenience. Let’s explore why:

Why Filing Online is Popular

E-filing offers numerous advantages over traditional paper filing, including faster processing and refunds, reduced errors, and the ability to file from anywhere at any time. Taxpayers receive a confirmation upon submission and can easily track their return status, enhancing transparency and efficiency.

IRS Free File and E-filing Options

The IRS offers several options to facilitate the e-filing process. IRS Free File allows eligible taxpayers to prepare and file their federal income tax returns at no cost using guided tax preparation software offered through a partnership between the IRS and the Free File Alliance. To qualify for IRS Free File, your adjusted gross income (AGI) must be $84,000 or less. The IRS Direct File program, launching more broadly in 2025, will be available to eligible taxpayers in 25 states. For those who don’t qualify for these programs, commercial tax preparation software remains a popular choice.

Overview of the Process

The e-filing process typically involves gathering necessary tax documents (like W-2s and 1099s), choosing your preferred filing method (IRS Free File, Direct File, or commercial software), entering your information into the chosen platform, and then electronically submitting your return. First-time filers over 16 using IRS Free File can enter “0” as their prior year income to sign their tax return.

Benefits of Filing Your Taxes Online

E-filing offers numerous advantages over traditional paper filing methods, making it a preferred choice for many taxpayers.

Faster Processing Times

E-filing significantly speeds up the tax return process. The acknowledgment of Income Tax Return (ITR) is quicker, and refunds, if any, are processed faster than with paper-filed returns. E-filed returns generally result in faster refunds, typically within three weeks, especially when opting for direct deposit. The IRS doesn’t have to re-enter your information into its system, decreasing the risk of delays.

Fewer Errors Due to Automated Calculations

E-filing software includes built-in validations and electronic connectivity that minimizes errors considerably. Paper filings can be prone to errors, and when paper-based forms are migrated to electronic systems, there’s a possibility of human error in data entry. Electronic systems curb this deficit through their tax calculation mechanisms, leading to increased data record accuracy. Built-in accuracy checks in electronic return preparation software catch most taxpayer errors before submitting the return.

Direct Deposit Refunds

E-filing offers the convenience of direct deposit for refunds and direct debit for tax payments. Taxpayers can even decide what day to debit their bank account for tax payments, among other convenience features.

Access to IRS Assistance Tools

While the search results don’t directly highlight access to IRS assistance tools as an exclusive benefit of e-filing, it’s worth noting that the IRS website provides various online resources and FAQs to help taxpayers navigate the e-filing process.

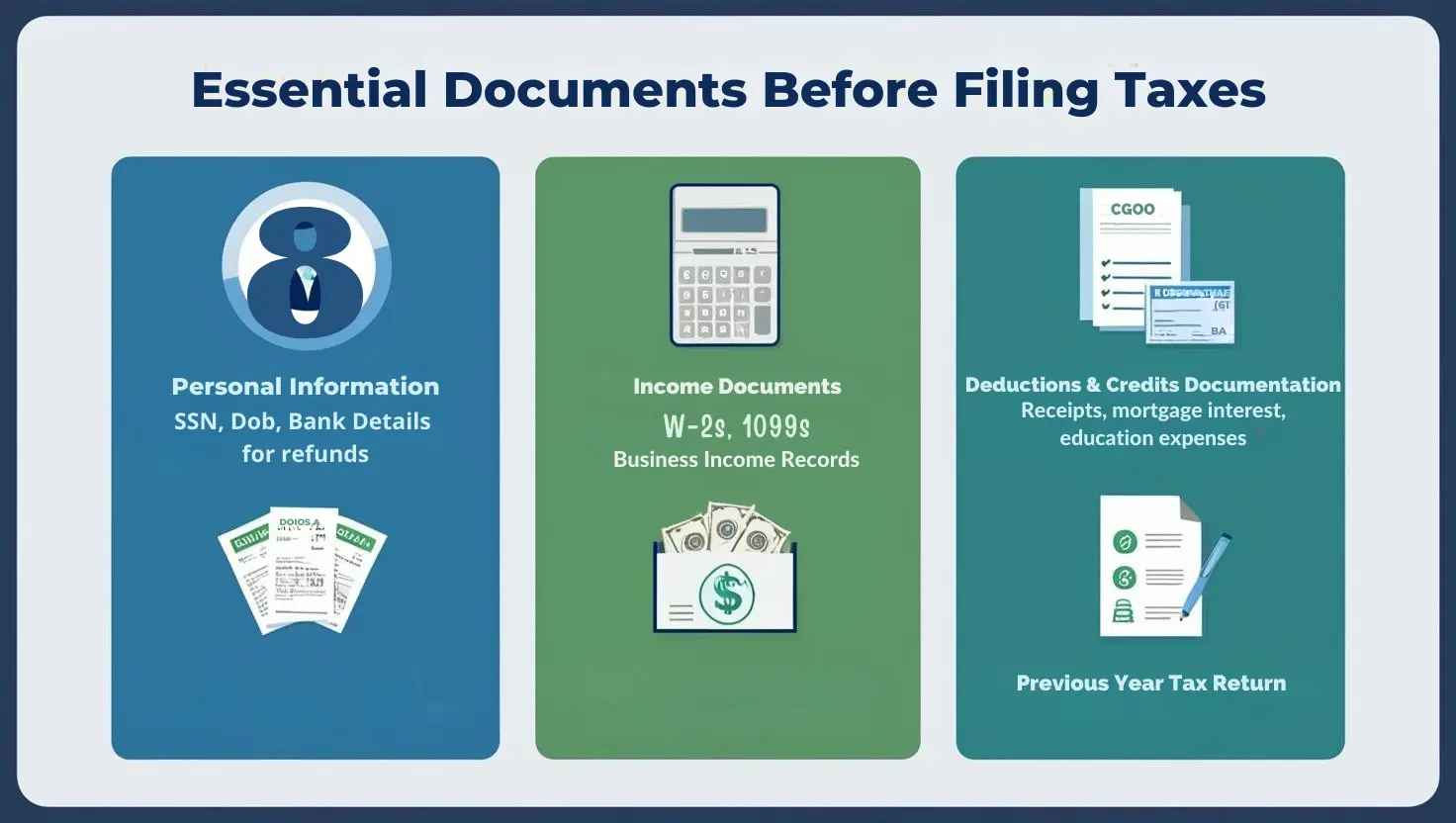

Documents You Need Before Filing

Before you begin the e-filing process, gathering all the necessary documents is crucial to ensure an accurate and efficient filing experience. Having these documents readily available will help prevent delays and potential errors.

Personal Information (SSN, DOB, bank details for refunds)

You must provide personal information for yourself, your spouse (if filing jointly), and any dependents. This includes Social Security numbers (SSNs) or Individual Taxpayer Identification Numbers (ITINs), dates of birth, and complete legal names. Additionally, you’ll require your bank account and routing number if you plan to receive your refund via direct deposit. Double-check these details for accuracy to avoid any issues with your refund.

Income Documents (W-2s, 1099s, business income records)

Accurate reporting of your income is essential. This requires gathering all relevant income documents, including:

- Form W-2: Received from your employer, showing your wages, salary, and taxes withheld.

- Form 1099: Received from various sources, such as banks (for interest income), clients (for freelance or contract work – 1099-NEC), or other payers. Different types of 1099 forms exist for different income types.

- Business Income Records: If you’re self-employed or own a business, you’ll need records of all income received and expenses paid. This might include invoices, receipts, and bank statements.

Deductions & Credits Documentation (Receipts, mortgage interest, education expenses)

To maximize your tax savings, gather documentation for any deductions or credits you plan to claim. This might include:

- Receipts: For charitable donations, medical expenses (if itemizing), and other deductible expenses.

- Form 1098: Showing mortgage interest paid (if you own a home).

- Education Expenses: Records of tuition payments (Form 1098-T) and student loan interest payments.

- Other Documents: Supporting documentation for any other deductions or credits you are eligible for, such as retirement contributions, energy-efficient home improvements, or childcare expenses.

Previous Year’s Tax Return

A copy of your previous year’s tax return can be helpful for several reasons. It can assist in verifying your identity when e-filing and provide a reference for income, deductions, and credits you may have claimed. The Adjusted Gross Income (AGI) from your prior-year return must often be signed and submitted electronically to your current year’s return.

Choosing the Right Tax Filing Software

The correct tax filing software is crucial for a smooth and accurate e-filing experience. Taxpayers have several options, each with its advantages and considerations.

Overview of IRS Free File and Commercial Tax Software

IRS Free File is a public-private partnership between the IRS and the Free File Alliance. It provides free tax preparation and e-filing services to eligible taxpayers. To access these free tools, taxpayers must start from the IRS Free File page on IRS.gov. The IRS Free File program offers two options:

- Guided Tax Software: For taxpayers with an Adjusted Gross Income (AGI) of $84,000 or less, this option provides guided tax preparation software from IRS partners. The software uses a question-and-answer format to guide you through the process, guaranteeing accurate math calculations.

- Fillable Forms: This option is available to taxpayers of any income level and provides electronic versions of IRS paper forms. It is ideal for those comfortable preparing taxes using IRS instructions and publications.

Commercial Tax Software: These are paid software options like TurboTax, H&R Block, TaxAct, and FreeTaxUSA. They often offer more features and support than the free options but come at a cost.

Comparison of TurboTax, H&R Block, TaxAct, FreeTaxUSA

While specific details about each software’s features and pricing change yearly, here’s a general comparison based on shared perceptions:

- TurboTax: Known for its user-friendly interface and extensive features, it can be one of the more expensive options.

- H&R Block: Offers a balance of features and affordability, with options for in-person assistance if needed.

- TaxAct: Generally, it is a more budget-friendly option for those with more straightforward tax situations.

- FreeTaxUSA: Offers free federal filing for simple returns, with affordable options for more complex returns.

Factors to Consider: Ease of Use, Cost, Support

When choosing tax filing software, consider the following factors:

- Ease of Use: Look for software with a user-friendly interface and clear instructions, especially if you’re new to e-filing.

- Cost: Compare the pricing of different software options, considering whether you qualify for free filing through IRS Free File. Some commercial software offers free versions for simple tax situations.

- Support: Check what support is offered, such as online chat, phone, or in-person assistance. Consider your comfort level with self-guided tax preparation and whether you need additional support.

By carefully evaluating these factors and comparing different software options, you can choose the right tax filing software for your needs and ensure a smooth and accurate e-filing experience.

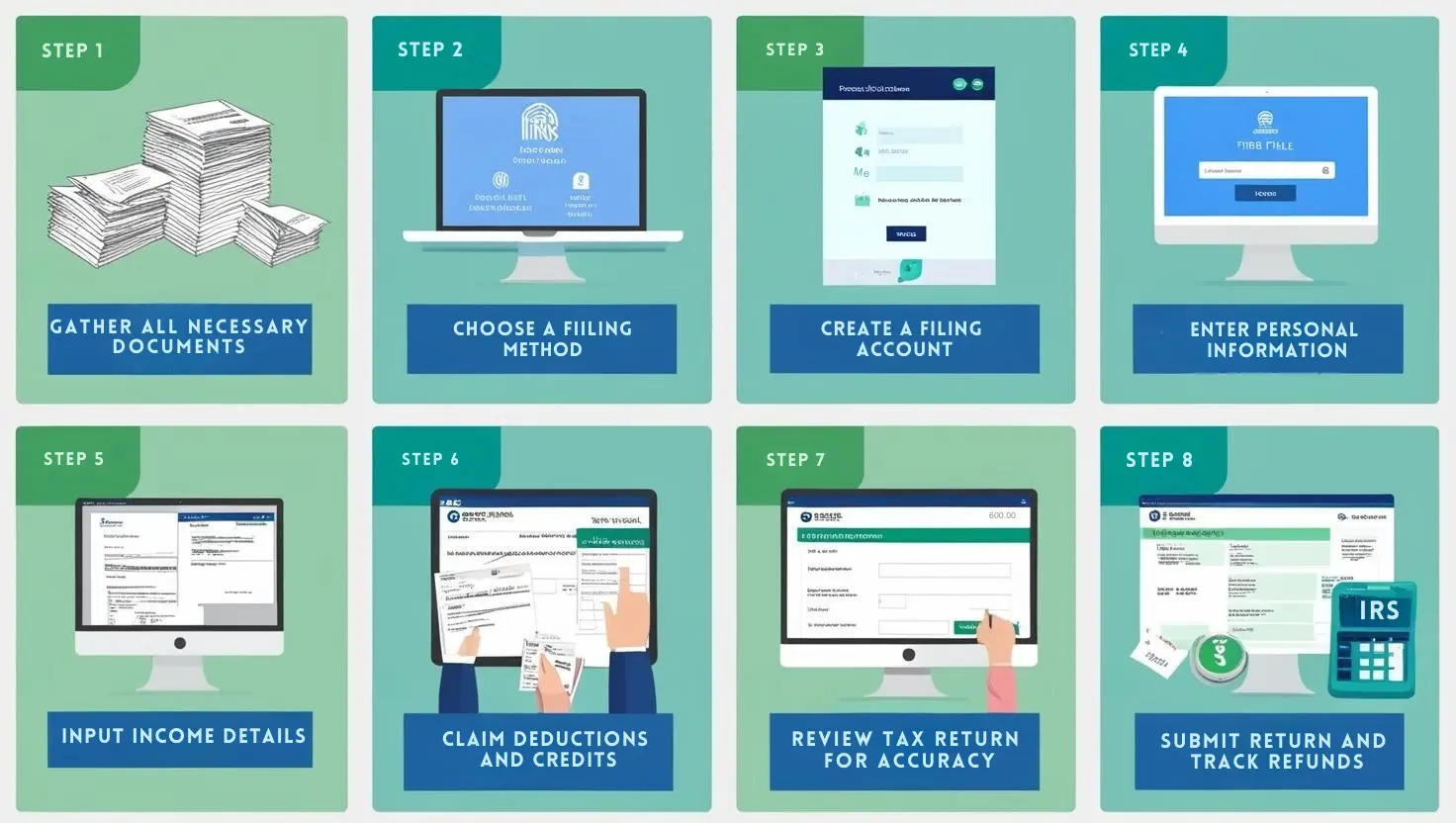

Step-by-Step Guide to Filing Taxes Online

Filing your taxes online can be a streamlined process if you follow these steps carefully:

Step 1: Gather All Necessary Documents

Before you begin, collect all the essential documents needed to accurately complete your tax return. These documents typically include:

- Personal Information: Social Security numbers (SSNs) or Individual Taxpayer Identification Numbers (ITINs) for yourself, your spouse (if filing jointly), and any dependents. Dates of birth are also required.

- Income Documents: Forms W-2 from your employer(s), Forms 1099 for various types of income (e.g., 1099-NEC for self-employment income, 1099-INT for interest income), and records of any other income sources.

- Deduction and Credit Documents: Receipts and records related to potential deductions and credits, such as charitable donations, medical expenses, student loan interest payments, and eligible educational expenses.

- Prior Year’s Tax Return: Having a copy of last year’s return can be helpful for reference and to verify your identity electronically.

Step 2: Choose a Filing Method (IRS Free File vs. Commercial Software)

Decide which method you’ll use to file your taxes online. Your options include:

- IRS Free File: If your Adjusted Gross Income (AGI) is below the threshold (typically $84,000 or less), you can use IRS Free File to access free tax preparation software from trusted partners.

- Commercial Tax Software: If you don’t qualify for IRS Free File or prefer a specific software’s features, choose a reputable commercial tax software like TurboTax, H&R Block, TaxAct, or FreeTaxUSA. Evaluate ease of use, cost, and support options when making your selection. IRS Direct File will be available to eligible taxpayers in 25 states.

Step 3: Create an Account on Your Chosen Platform

Visit the website of your selected platform (IRS Free File through IRS.gov or a commercial tax software provider) and create a new account or log in to your existing account. You will likely need to provide your email address and create a secure password.

Step 4: Enter Personal Information

Carefully enter all required personal information, including your name, address, Social Security number, and date of birth. Ensure that this information matches your official documents to avoid potential issues with your return.

Step 5: Input Income Details (W-2s, 1099s)

Follow the software’s instructions to enter your income information accurately. Input the data from your W-2 forms, 1099 forms, and any other relevant income documents.

Step 6: Claim Deductions and Credits

Review the available deductions and credits and determine which ones you’re eligible to claim. The software will typically guide you through this process and ask questions to help you identify potential deductions and credits. Enter the necessary information and documentation to support your claims.

Step 7: Review Tax Return for Accuracy

Before submitting your tax return, carefully review all the information you’ve entered to ensure accuracy. Check for any errors or omissions. The software will usually have a review feature that highlights potential issues.

Step 8: Submit Return and Track Refund

Once you’re confident that your tax return is accurate, follow the software’s instructions to electronically sign and submit it. You’ll typically need to provide your prior-year Adjusted Gross Income (AGI) or create a self-select PIN to electronically sign. After submission, you’ll receive confirmation that your return has been accepted. You can then track the status of your refund using the IRS’s “Where’s My Refund?” tool on IRS.gov.

Understanding Tax Deductions & Credits

Tax deductions and credits are essential components of tax planning that can significantly reduce your tax liability. Understanding the difference between standard and itemized deductions, as well as the various tax credits available, can help you optimize your tax return.

| Criteria | Standard Deduction | Itemized Deduction |

| Definition | A fixed dollar amount set by the IRS based on filing status. | Deductions based on specific eligible expenses. |

| 2024 Standard Deduction Amounts | Single: $14,600 Head of Household: $21,900 Married Filing Jointly: $29,200 | Deductions based on specific eligible expenses like medical costs, mortgage interest, and charitable contributions. |

| Additional Deduction for Seniors/Visually Impaired | Yes, additional deduction available. | Not applicable directly, but specific deductions may still apply. |

| Common Itemized Deductions | N/A | Medical expenses, mortgage interest, state & local taxes (up to $10,000), charitable contributions. |

| Form Required | Form 1040 (Automatic) | Schedule A of Form 1040 |

| Paperwork & Record-Keeping | Minimal | Extensive; must keep records of eligible expenses. |

| Best Choice Depends On | If the standard deduction is higher than total itemized deductions. | If total itemized deductions exceed the standard deduction. |

| Impact of Tax Cuts and Jobs Act (2017) | Nearly doubled standard deduction, making it more beneficial for many taxpayers. | Eliminated or capped many itemized deductions, making standard deduction preferable for many. |

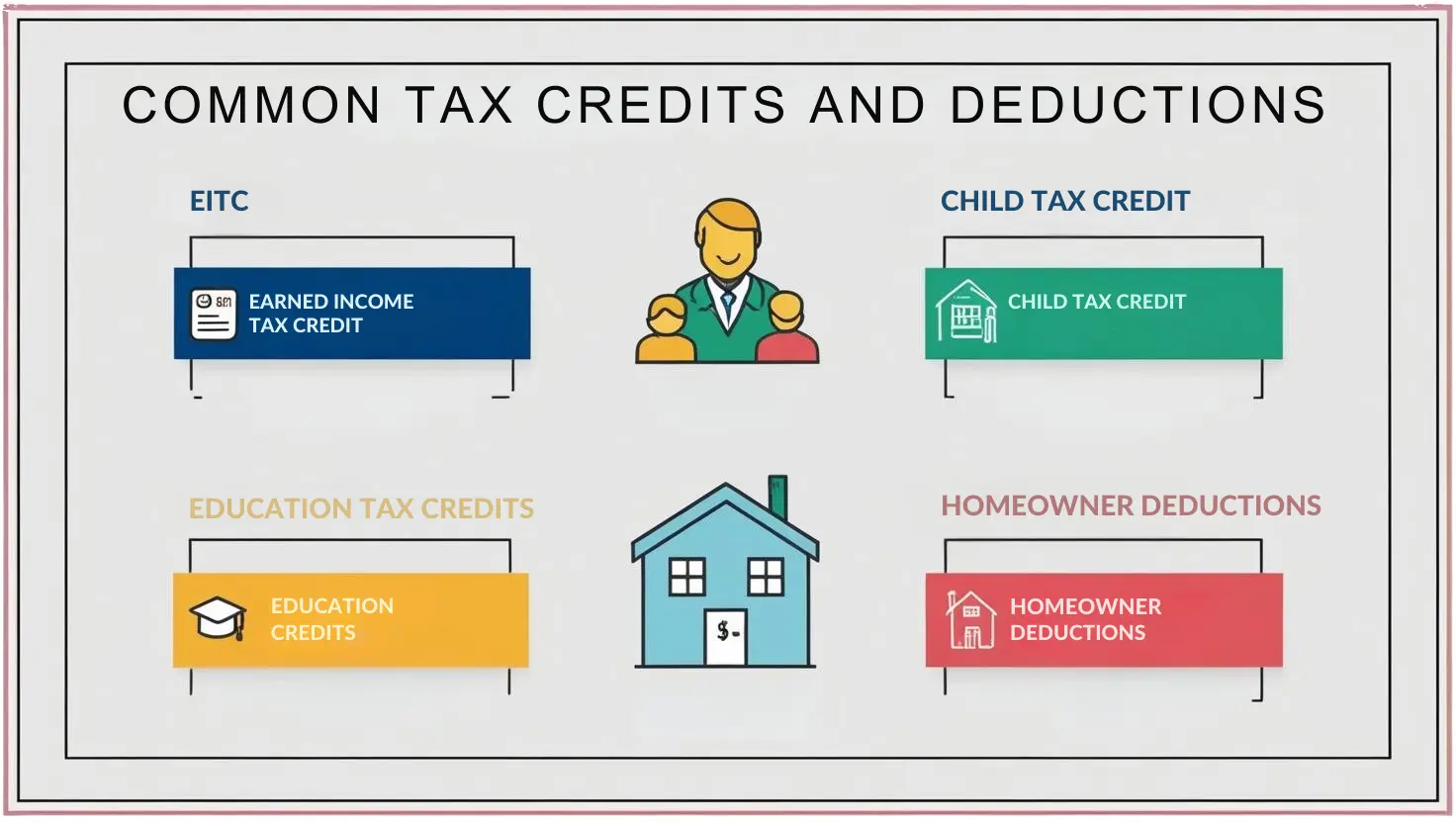

Common Tax Credits

Tax credits directly reduce the amount of tax you owe, providing a dollar-for-dollar reduction of your tax liability. Here are a few common tax credits:

- Earned Income Tax Credit (EITC): Designed to benefit low- to moderate-income workers, the EITC allows eligible individuals to reduce the taxes they owe and potentially increase their refund. Eligibility and credit amount depend on income, filing status, and the number of qualifying children.

- Child Tax Credit: This credit provides financial relief to families with qualifying children under the age of 17. For the 2024 tax year, the credit amount is up to $2,000 per qualifying child. The credit phases out for higher-income families.

- Education Credits: The IRS offers two primary education credits

- American Opportunity Tax Credit (AOTC): Provides a credit of up to $2,500 per eligible student for the first four years of higher education.

- Lifetime Learning Credit (LLC): Offers a credit of up to $2,000 per tax return for qualified tuition and related expenses, applicable to undergraduate, graduate, and professional degree courses.

- Homeowner deductions (mortgage interest, property tax): Homeowners may be eligible for deductions that can reduce taxable income:

- Mortgage Interest Deduction: Allows taxpayers to deduct interest paid on mortgage debt up to $750,000 for homes purchased after December 15, 2017.

- Property Tax Deduction: Taxpayers can deduct state and local property taxes paid during the year. However, the total deduction for state and local taxes, including property taxes, is capped at $10,000 per return.

Understanding and utilizing these deductions and credits can lead to substantial tax savings.

Read part II here:

A Complete Guide to Filing Your IRS Tax Return Online: Part-II